Where the strategies

come

from...

IDEAS, ANALYSIS, AND EXPERIENCE.

An Easy Guide to Choosing the Right Content for Financial Professionals

Are you having a hard time getting started with creating online content? Fear not! Try treating your content creation process more like a conversation and you will have an easier time.

One of the most frequent questions I hear from financial professionals and marketing leaders in the industry is "What type of content should we publish?"

It's interesting, this "What should I say?" question is a challenge many people face throughout their lives. I thought about how common it is this weekend when I was giving my 13-year-old son some guidance about starting his blog. He has a passion for Disney and I suggested he start a blog to begin to share his thoughts and build an audience.

Every day my son will share some "little-known fact" or something he read about Disney or Disney World with us and yet when it came time to start his blog he had writer's block. How is it possible that someone who is so passionate and talkative about a topic can freeze up when it comes time to share his thoughts with the world?

It's simple. He's thinking that he has to create a masterpiece that will shake the world. He, like many of the financial professionals I have guided over the years, is also afraid of his content being criticized.

It is interesting however that this expectation of greatness or fear of criticism rarely seems to arise when one is having an in-person conversation. Why? Because conversations are a regular part of life. You simply move from one conversation to another with ease. Some are really good and meaningful, some are bad, but most simply fade away after they have run their course.

Think of Content Creation as a Conversation

Approaching content creation as a conversation takes the pressure off and it makes it easier to connect with your audience. Speaking of your audience....

Who Are You Having a Conversation With?

There is a reason why every engagement we have at finservMarketing starts with an exploration of the client's target market. We need to know who it is we are talking to. This helps us frame our approach to the conversations we will have with them. Think about it, if you target high-tech professionals you are going to have a different set of conversations than you would if your target market is auto repair shop owners.

What do people in your target market like to talk about?

This sounds like a basic question but it really helps to keep it in mind. People in the tech space love to talk about startups, new innovations, the futures, stock options, venture capital, and so one. While people in the auto repair business have a whole host of other topics or interest or concern to them. Invest some time listening to your target market and approach your content strategy with their interests in mind.

How Do You Want To Influence Their Thinking And Behavior?

There are three primary goals for content marketing:

- Win New Clients

- Expand Client Relationships

- Keep Clients Longers

Each conversation you have with your clients, prospects, and referral partners offline serves to influence one of these behaviors whether you are actively thinking about it or not. Whenever you are talking to someone you should be thinking about bringing on new business, increasing the share of wallet you have with existing clients, or retaining clients longer. Keep this in mind when you are creating content online and it will give you great clarity.

There Are Only Three Things You Can Do In a Conversation

"What?! Only three?! Are you sure?" Okay...technically you can leave a conversation but that would be the opposite of content creation so it really doesn't count in this context. As far as content creation is concerned there are only three things you can do. All you have to do is choose one and proceed.

1) Start a Conversation

You do this all the time. You decide that you have a question to ask or a topic you would like to cover and you start talking. You can do the same with your online content. Think about the blog post you are reading right now. This is an example of a conversation starter. I wanted to talk about something that I think is important to you and other members of my audience. So, I sat down and started typing. I hope you find it interesting and it will cause you to...

2) Join the Conversation

If you are like the majority of people living in the digital world you are likely spending a lot of time consuming content online. Whether it is on Facebook, LinkedIn, Twitter, Instagram, YouTube, podcasts, or elsewhere. Here's a trick, when you see something interesting join the conversation by writing about it, recording a video or podcast, or simply share it with your audience with a quick comment to introduce the conversation to them.

There is a never-ending stream of content being produced and distributed online. You don't have to be the one who starts every conversation. Sometimes you can add more value by curating the good stuff and adding your two cents.

3) Change the Conversation

Sometimes...okay often times... people are focusing on the wrong thing. Maybe it's taxes or Bitcoin or what the Fed is doing with rates. Whatever it is, you can do your audience a great service by steering the conversation back to what's really important to them. As a trusted advisor to your clients, you have the ability to influence their thinking and behavior in ways that help them achieve their goals. When you see the conversation going in the wrong direction you can help keep them on track.

Think about your time online as being similar to attending a networking mixer. You are going to be in an around a lot of conversations. The goal isn't to be a genius. It's to be relevant. You want people to see you, recognize that you had something interesting to say, and remember you when the time is right.

Was this helpful? Did I miss something? What are you thoughts? Let me know in the comment section below.

Is Cold Calling the Marketing of Last Resort?

Does your business rely too heavily on cold calling to generate new deals? If so, read this post to explore some ideas on how to improve your odds of success.

I was having a beer with my friend Garrett on Friday and we got to talking about the new marketing program that I recently launched for ISOs and brokers in the alternative lending space. He heads up marketing for a relatively large investment firm here in Austin so I was interested to get his take.

During our previous get together I had told Garrett about merchant cash advances, in the context of the work I have done with Pearl Capital, so he had a high-level understanding of the market. He was blown away by how much ISOs and brokers can earn from MCA deals.

"What?! How is it possible that the commissions are so high?" he said.

Commissions north of 5% died out in the investment industry back in the 1990s with the dawn of online discount brokerage firms so he just couldn't understand why ISOs are paid so much. However, when I explained that for many small business owners an MCA is a funding option of last resort he got it. There simply is no other viable option available for them on such a short time frame. As a result, the capital is expensive and the competition for deals is high so companies like Pearl are willing to pay ISOs generously for funded deals.

So, when I told Garrett that the primary mechanism many ISOs use for sourcing deals is cold calling business owners from purchased lists he kind of laughed and said:

“Cold calling? Isn’t that the marketing of last resort?”

Photo by Hannah Wei on Unsplash

Ha ha ha! We both laughed but we knew he was only “kinda” joking.

In my experience, cold calls aren’t the marketing of last resort. Sadly, for most financial professionals cold calls are the marketing of first and only resort.

Here’s the thing. Cold calls do work but they take a lot of effort, time, and patience. As I wrote in an article for Pearl, successful cold calls require almost perfect timing. It also requires a set of skills that most people don’t have.

If cold calls are your primary mechanism for generating new business you are working way harder than you need to and you are almost certainly dealing with a lot of low-quality leads.

Expected Success Rate for Cold Calls

When was the last time you made a purchasing decision based on a cold call? If you’re like most people the answer is never.

If you have ever made a purchase based on a cold call was it a major financial decision? Probably not. And therein lies the challenge you are facing as a financial professional. Cold calls are not the best marketing mechanism for selling financial products. Whether it's an MCA, insurance policies, or investment products.

Effective Marketing for ISOs and Other Financial Professionals

Understanding that cold calls, in most cases, aren't actually marketing at all. They are unsolicited sales calls. Sure, occasionally you will get lucky due to the law of large numbers and someone will say yes but let's be honest that's a rare event.

Effective marketing seeds sales by attracting your target market to a marketing funnel that allows prospects to reveal themselves to you. Think of it as process that encourages someone to raise their hand to say "I think I need what you sell."

Does this mean that you should abandon cold calls? No, not 100%. But, I would recommend two things:

- Shift to Warm Calls - Get focused on a specific target market so that you are calling people who are likely to appreciate your specialization.

- Create a Call Scheduling Process - Invest in the development of a process that encourages members of your target market to book a call with you. There is a world of difference in a call that the prospect has scheduled with you versus the one where you called the prospect out of the blue.

Hopefully you found this interesting. If so, leave me a call or questions. I would love hear from you.

How to Get People to Share Your Content On Social Media

People's social media streams are noisy. But getting your friends, fans, and followers to share your content isn't impossible. You just have to hit the right emotional triggers.

Want people to share, retweet, or forward your content to their network? Make sure it hits an emotional trigger.

One of the most commonly overlooked components of effective social media marketing is the emotional response of your network.

If I had a dollar for every time I heard a financial advisor, agent, or wholesaler tell me "I've tried social, but I haven't seen any results." only to look at their social media actively to see nothing but bland updates about the markets and almost zero human engagement.

Do you want people to engage with your content? Share engaging stuff!

The infographic below, produced by CoSchedule, does a fantastic job of laying out the "Psychology of Social Sharing" by hitting the major reasons why people share content via social media.

Looking at the list you may notice that there is not category for "economic updates" or "interesting financial information." Does that mean you shouldn't share those things? No, of course you should. But you should package them in such a way that they hit at least one of these triggers.

Infographic by CoSchedule: http://coschedule.com/blog/why-people-share/

Want to update people on what's happening in markets or answer general financial questions for people?

Try using the approach that my friend Kathryn Cicoletti uses in her MSB Cheat Sheet series. In the example below she explains the difference between an individual bond and a bond fund. She tosses in a little comedy and breaks up the talk with some text and graphics.

What emotional trigger(s) is she hitting? Entertainment and Self Fulfillment for sure. The video is a great way to enjoy (be entertained) while learning something new.

Hint: Video is a fantastic way to get people to share. Your clients and prospects love video. Notice that Kathryn is shooting this video solo at her desk/table. It's not a difficult as it seems.

The takeaway?

Think about your reader/viewer/listener before you share content. What emotional response will they get when they experience what you've shared? If you can't think of one, consider repackaging the content so that it's more engaging.

Video Captivates Your Clients and Prospects Like No Other Medium

The average American watches over 42 hours of video each week. Yet, most professionals are using little, if any, video in their marketing and communications efforts. This is a problem.

How many hours of video have you watched in the past week?

Chances are you have consumed over 40 hours of video in the past week. According to Nielson’s Q1 2015 “Total Audience Report” the average American adult watches over 42 hours of video each week when you combine TV, PC, smartphone, and tablet viewing.

People spend the equivalent of a full-time job each week watching video!

Let that sink in for a moment….

Your clients and prospects love video so much that they consume video content to the tune of 6 hours each day. That’s kind of amazing when you consider that, according to a 2013 Gallup survey, the average American only clocks 6.8 hours of sleep each night.

Knowing this, it begs the following question.

How much video are you producing for your clients and prospects to consume?

If a prospect told you she was a vegan would you take her to a steakhouse for a dinner meeting? Of course not. Yet, if we did an audit of the digital content you and your firm routinely share via email, your website, and social media channels my guess is almost all of it is text based. There’s nothing wrong with text, people still read. It’s just that we know for certain that your prospects and clients love video. So why not share information with them in their favorite format?

There are two primary objections I hear most from clients when I suggest adding video to their marketing and communications mix. One is cost and the other is fear of making poor quality video. Let’s tackle both real quick so you don’t fall victim to them:

- Production Cost - If you have a smartphone and access to a reasonable quiet space with good lighting you’ve got yourself a production studio for almost $0.

- Your phone, if it was made in the last 3 years or so, can shoot in full HD and there are hundreds of video apps available on iOS and Android that are free or cost $10 or less.

- Distribution is also free or extremely low cost. Simply publish your video to YouTube, Vimeo, Vine, Instagram, or live stream it via Periscope, Meerkat, or Ustream. You can even post video directly to Facebook and Twitter now. Again, most of these options are free.

- If you want to spend some money on higher-end equipment you can get all you need including studio lights and miss for under $2,000 if you spend right.

- So, cost isn’t really a legitimate roadblock. If you are a professional in 2015 and beyond you should have video production capabilities.

- Production Quality - As I mentioned above, a quiet space, good lighting, and your smartphone will actually produce very high quality video at almost no cost. The question of quality for most clients (particularly financial advisors and other professionals) is really a fear of looking bad in front of their clients. We’ve all seen cheesy videos and no one wants that. Here are a few things that will help avoid making poor quality videos:

- Smile and talk to the cameral like you are talking to a real person. If you are engaging and approachable your clients and prospects will love it.

- Focus on video platforms where the viewer expects video with minimal or zero post production (editing). My personal favorite (as of this writing) is Periscope. It’s a live streaming app for iOS and Android that allows viewers to comment and ask questions while you are broadcasting. The fact that it’s live and interactive eliminates the fear of it needing to be “studio quality” and it offers you and your viewers a super high-touch experience.

- Pump up the volume! Produce video regularly, as part of your routine. Get in the habit of using video as a means to expand your influence and engage with clients. The more to you do it the better you’ll get and as a result the quality of your content will improve.

Note: Periscope is also one of the fastest growing social networks in history. Our “Periscope for Professionals” course offers several tips and tricks for getting started with the app and its social network. The course also covers recording for compliance and several use cases for your business.

The next generation expects video and will seek it out over print.

Eric Guerin of Adelie Studios wrote a great post about "Marketing to Millennials" and he lays out the case, with tons of supporting stats, that video is the most compelling medium for the millennial audience. It makes sense, the millennial generation are the first digital natives.

This next great, gold rush generation of clients has never known a world without online video. They have no idea what the “test signal” looked like on TV because they’ve always lived in a world with 24/7 cable television. They have no memory of a world before sports bars with flat screens everywhere. To them, watching videos on their smartphones while on the toilet is something they’ve been doing since high school.

YouTube is a viable search engine for your next generation of clients. Will they find you there when they search for their next big financial question? I hope so.

The big takeaway is obvious.

Start producing and distributing videos for your clients and prospects. Share them on your website, via your newsletter, YouTube, Facebook, Periscope, and whatever platform they are using. It’s just smart business.

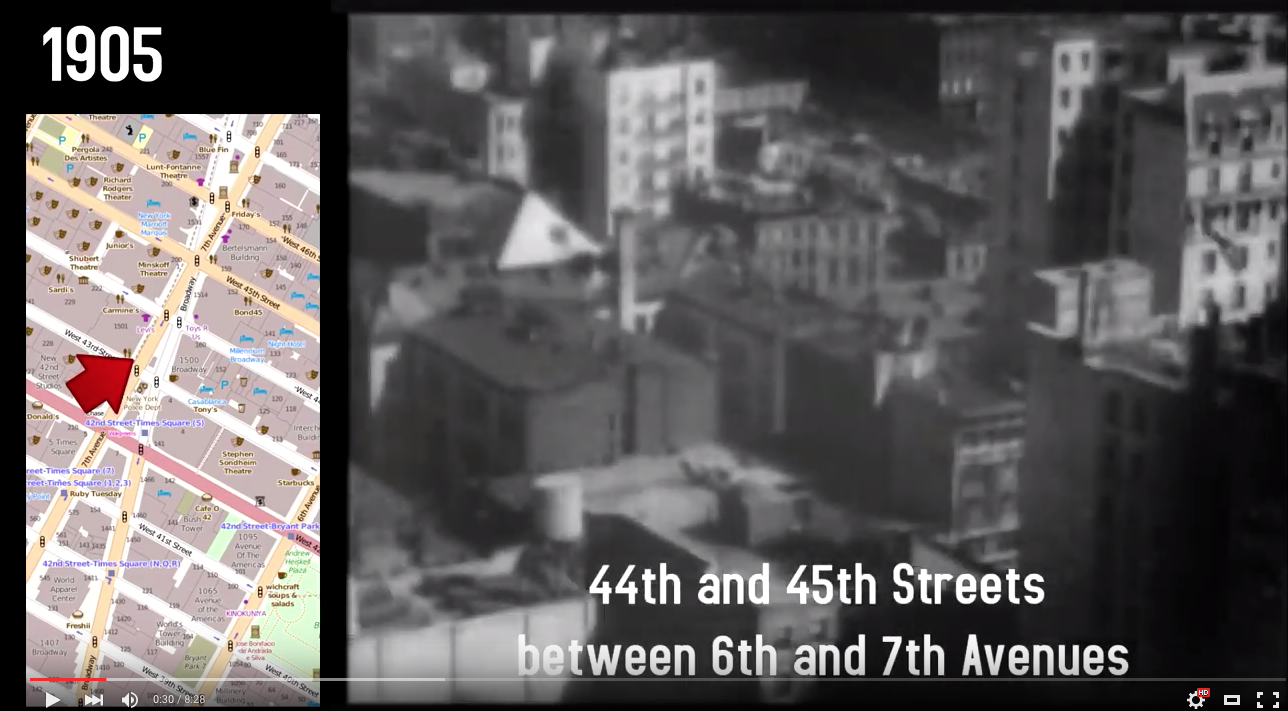

BONUS: Below is what is claimed to be the oldest video footage of New York City. These video clips are from 1903 and 1905. Once you start watching it, I assure you you’ll be hooked. Like I said, video captivates like no other medium.

The oldest and most incredible footage of New York City ever, including where the WTC would be built. With added maps carefully researched to show where the camera was. 28 shots of classic footage with a new twist and a new soundtrack.

The Long Awaited Return of Twitter's Google Juice Is Here

I joined Twitter back in October of 2007 at the urging of a PodCamp Boston presenter. For several months after that I failed to see the value in the service. My "Ah ha!" moment came when I noticed one of my friends had added a link to his Twitter profile on his email signature and I decided to explore why he would such a thing.

PodCamp Boston

— Mike Langford (@MikeLangford) October 27, 2007

When I checked his Twitter profile I noticed that he had accumulated 600 followers. Then I googled his name. Sure enough, a link to his Twitter profile popped up on the first page of results. As I started to poke around a bit more I realized that each tweet created a unique URL. So, Google was indexing every single tweet as it would for any other page of content on the web. I immediately got it. I thought to myself:

Whoa! Twitter is Google juice!

That's right, every tweet a user posted had the potential to show up in someone's search results. That made Twitter extremely useful as a publishing tool.

Sadly, in July of 2011 Twitter decided it didn't need Google anymore for search and ended the tweet indexing relationship. At the time Twitter was riding high and some people were predicting that its real-time search results were going to put a serious hurt on Google's bottomline.

How has Google's stock performed since Twitter canceled their tweet indexing relationship in July 2011? The chart above tells the story.

Now that Twitter is a public company and scrambling to onboard new users and keep existing users engaged, they have decided that having tweets display in Google search results might not be such a bad idea after all. (Note: This is just my analysis of Twitter's likely motivation. There have been rumors that Google is in talks to acquire Twitter due to, what is considered by many as, a failure of Google+ to catch on.)

So what does the impending reappearance of tweets in Google search results mean for you and your business?

- Everyone can see your tweets. The big appeal of Twitter, for business, is that tweets are public people can view them and subscribe to your account with ease. The problem is not that many people actively use Twitter. A newly released Pew Research study of American social media usage revealed that only 8% of American adults use Twitter daily. (Note: 23% of American adults use Twitter. Only 36% of these people use the service daily. 23% * 36% = 8%) The average person simply has no real need for Twitter when they have Facebook for social. However, everyone uses Google. Once the tweet indexing is reactivated you can expect your tweets to reach a much wider audience.

- The SEO value of your tweets matter. There's only so much real estate on the first page of Google results. If Google is going to start displaying tweets there you want to be sure yours display where and for whom you would hope they would. Keywords, time, date, location, the size and relevance of your Twitter network, and the engagement of your tweets are likely to impact whether your tweets or someone else's display as a result for a given search.

- Search Plus Your World is likely to be really important. About a year after Twitter terminated the tweet indexing relationship Google launched Search Plus Your World which allows you to see search results based on stuff your friends have shared on Google+ or YouTube. When Google announced the service they said they were open to including other social network results but Twitter declined. With the Twitter relationship rekindled it's a sure bet that who follows you and/or has your Twitter profile in their Google contacts will play a big role in what results display when they use the search engine.

The takeaway, Twitter might become much more important to your digital marketing strategy in 2015 and beyond. It's probably a good idea to start thinking about how you and your team will adjust your efforts.

How to Differentiate Your Financial Practice Online

It's easy to stand out in the crowd when you choose the crowd.

Sometimes it's the little things that cause us the most consternation in our businesses. Of course these little things don't feel so little when they are plaguing our minds and holding us back from achieving our goals.

I've seen the little details hold financial professionals back from fully committing to using social media in their practice more times than I can count over the years. The little things range from "I don't know what to post." to "I'm not sure I can be myself on Facebook if I'm connected to my clients." to "What if someone says something bad about me online?" and beyond. While these little things may seem trivial to you as you read them I promise you they are holding back many well established, seasoned professionals from embracing digital marketing.

Yesterday I was reminded of another little thing that I have heard frequently while working with financial advisors, insurance agents, and wholesalers. Blane Warrene, of QuonWarrene, while attending the Morningstar Investment Conference tweeted "Number one question first day of social media lounge at #MICUS - "so many on social now - how do we differentiate?" cc: @MStarAdvisor".

Number one question first day of social media lounge at #MICUS - "so many on social now - how do we differentiate?" cc: @MStarAdvisor

— Blano (@blano) June 19, 2014I had heard this concern in the past mainly as a negative reaction to the canned content libraries that many large financial firms require their financial professionals use to post to their individual social media accounts. The common lament was "How do I stand out when thousands of other advisors are posting the exact same thing to their accounts?"

While the "How do we differentiate?" question Blane reported is a much deeper concern than the frustration of having little to no flexibility in what you can publish the solution is the same.

Focus On A Niche

The challenge of differentiation in terms of your brand or the content you share is easily resolved when you focus on a specific target market. It sounds insanely simple but this fundamental business concept is the most powerful thing you can do to stand out from the crowd.

Why? Because with a niche you are playing to a specific crowd. When you refine your target market you build your network of connections on LinkedIn, Twitter, Facebook, Google+ and beyond in custom fashion. Your audience is no longer the same as your competitor's so you free yourself from the anxiety of differentiation and focus on sharing content that resonates with the people you have chosen to serve.

Who cares if another guy shared a link to the same content with his followers? Who cares if every other financial advisor in the country has access to the same stocks, bonds, mutual funds, and insurance products as you do? You only care about your followers, the people on your email list, and the visitors to your site.

Focus on sharing content that is interesting, relevant, and useful to your target market and you will never have to worry about a little thing like differentiating yourself online.

The Formula for Calculating the Expected ROI of Social Media for Financial Advisors and Insurance Agents

The “What's the ROI of social media?” question has been a topic of debate, analysis, and discussion ever since marketers started making the case for the business use of social networks. The reason the conversation on social media ROI persists is that for most businesses it is relatively difficult to get even a reasonable approximation of the true financial impact of social.

That’s why Gary Vaynerchuk’s famous “What’s the ROI of Your Mother?” portion of the talk he gave at Inc 500 in 2011 resonated so loudly throughout the digital marketing community and is still referenced today. Social media marketing, by its very nature, is about interacting with people and there will be a lot of time and energy invested in what may often look like non-business related engagement. This is no different than going to real life networking events or belonging to a local BNI or Rotary Club chapter. In these offline social networking activities, you know that you will eventually get new business from them but you just don’t know exactly when or how much business that may be. Yet, very few financial professionals question the value of networking time invested within their local community.

In my experience, the reasons many financial advisors and insurance agents question the ROI of social media in their practice are a sense that their target market isn’t using social and the belief that social media usage will be a huge time suck. The first objection is an easy one to overcome with data. Over 70% of all adult Americans use social networks regularly and the numbers get much higher than that in younger segments. More importantly, 90% of high net worth individuals are using social routinely. The time objection is really a lack of appreciation for the value potential of social media usage. If advisors and agents really knew how many potential new clients and how much impact regular engagement with their existing clients might have on their book of business they’d make it a priority.

In this post, I am going to share a simple formula with you for calculating the expected ROI of your social media engagement as a financial professional.

The “as a financial professional” caveat is there for a very specific reason by the way. Most of what is written about social media ROI is written for marketers at large brands or enterprises that are dealing with customer populations in the tens of thousands or even millions. But as a financial advisor or insurance agent, your business is unique to you. You are the brand. Your clients are doing business with you. Even if you work for a large wirehouse or are affiliated with a larger firm the client sees you as their “guy” or “gal”.

While the big brands and enterprises talk about "client relationships" and "engaging with the customer” you live and die by relationships. And social networks like Facebook, Twitter, LinkedIn, Google+ and so on are the most powerful relationship management tools in the history of business. It’s the power of these tools to make it efficient for you the advisor or agent to manage a very large number of relationships with prospects, clients and referral partners that makes it easy to craft a predictive model for the financial return you’ll see from your social media efforts.

The formula looks like this:

- C x E% x W% x R x Y = Revenue

- T + P + Ed = Investment

- (Revenue - Investment) / Investment = ROI

Before we move on the components of the formula I want to touch on one thing real quick. There is a legitimate case to be made that ROI is not an appropriate measure for evaluating social media marketing spend. The reason being is marketing is an expense, not an investment. Sean Jackson, CFO of Copyblogger, co-wrote a fantastic post titled "There is No ROI in Social Media Marketing” that really articulates argument well. You should read it. As a financial professional you’ll love it. But…finish reading this post first because this one is going to make a huge impact on your business.

Okay…onto the formula components for your social media ROI calculation:

C = Connections

Connections are what make a network work. Especially connections to people in your target market. The expected value of your social media marketing efforts is driven mostly by the quality and scale of the network of connections you have. It sounds so obvious but you would be absolutely amazed at how often I have heard a financial professional tell me that “social media just isn’t working for me” and I take a look at their LinkedIn, Twitter, and Facebook profiles and none of them have more than 100 connections. If you want to build a large book of business you are going to have to connect with people. Lots of people. Lots of high-quality people.

If you are an adult living in America you have almost certainly met thousands of people over the course of your life so far. Many of those people are high-quality connections who may someday be in the need of your services as an advisor or agent. Many more will have the opportunity to refer business to you. The easiest way for these people to stay connected with you and for you to not lose touch with them is to connect with them via their preferred social network.

Size matters when it comes to your network. You would never think that you could build a profitable book of business by sending a mailing to only 100 people or only talking your close friends and family right? Of course not. Success with social media begins and ends with your network. Make it a serious priority to add lots of high-quality connections.

E% = Events Percentage

The business of financial advisors and insurance agents is largely event driven. As I have often said from stage when speaking to financial professionals:

Not everyone you meet is in the market for your services right now. But eventually most of them will be. So you need to be paying attention to their life to notice when those events happen.

People use social networks to broadcast major life events to their connections. Sure there’s a lot of selfies, food porn and cat videos but the money in motion events are there too. Your connections will update Facebook, Twitter, LinkedIn, Google+ and more with news of job changes, marriage, divorce, new babies, new homes, new cars, death in the family, and just about any other major life event you can imagine. You have the ability to be in the loop for every potential 401k rollover, 529 plan or insurance policy needed simply by connecting with people via social networks and paying attention.

The paying attention part is important. Digital marketing professionals call this part “listening.” You are listening to your network for updates that indicate a need for your assistance.

Now, the reality is not every member of your network is going to have a money in motion event each year. Some percentage of your network will, however. What that percentage is will vary by network composition. Certain segments might change jobs more frequently or be in prime childbearing years while others might be in pre-retirement. But you can make an assumption and test it against actual activity over time. For example, you might assume that 20% of the people you are connected with will change jobs in a given year. Seem too high? Too low? You can test it via LinkedIn’s Year in Review application. When I run it for my network I see that 203 people out of the 959 that I am connected to on LinkedIn changed jobs or got promoted at work. That’s about 21%.

Assuming an even distribution across a 48 work week year that would be 4 prospects to reach out to per week about a potential 401k rollover, financial plan, or discussion about life insurance. How would your business change with four new qualified leads per week?

Of course, we know that you aren’t going to win the business of all of these people with life events in a given year. Some will already have an advisor or be “all good” with insurance. Some will not be the right clients for you because they fail to meet your asset minimum. This leads us to the next formula component.

W% = Win Percentage

What is your win percentage? How often do you convert a prospect into a client? Here again it is going to vary based on the quality of your network and your ability to close business.

Let’s say that 50% of the people who have money in motion events in your network are true prospects and are in the market for the services you provide. Great! Now, let’s say that you have an average close rate of 50% on qualified prospects. This translates into a win percentage of 25% on connections with money in motion events discovered via social media. If we continued my LinkedIn Year In Review numbers from above we would expect you to close 25% of the 203 people who changed jobs during the year resulting in about 51 new client relationships for the year.

Now things are starting to get exciting. But how exciting? Let’s go to the next formula component to put some dollar signs on this opportunity.

R = Revenue Per Client Annually

In this formula component, I am going to keep things really simple to make it easy for you to convert the math to your revenue model. There are just far too many fee and commission schedule variants in the financial industry to cover. I’m going to use an asset management fee approach that is common for RIAs which is what I am most familiar with given my background in investment management.

Let’s assume that each new client, on average, will open an account with $100,000 and you earn 1% annually on assets under management. That’s a revenue stream of $1,000/year for each new client. It’s a small amount but again, adjust as you see fit.

Y = Years Per Client

Most financial clients have a multi-year lifetime relationship with their chosen financial professional. If your business is transactional in nature this number would be 1. But for most advisors and agents client relationships will continue to generate revenue annually.

Here again you will need to make an assumption or use actual numbers from your practice. I am also going to keep things super simple and avoid using a net present value of an annuity stream for this number. Feel fee to do that if you want but personally I don’t think that level of precision is needed in this process.

Let’s assume you keep a client for 7 years on average. I chose that number because I used to work for a very large financial firm with a huge retail client population and that was average client lifetime according to actual data over 60+ years and millions of clients. Results may vary on your end.

Revenue

Okay, here we go…ready?! Below is the revenue formula based on the numbers I shared above.

959 Connections x 21% Events x 25% Win x $1,000 Revenue Per Client x 7 Years = $352,432 in New Revenue

Key things to remember:

- This is the result of your first year’s efforts with social media marketing.

- Imagine how your practice might be transformed over the course of a few years.

- We are keeping things super simple here and avoiding any discussions about social media strategy and tactics.

- If you want to learn how to make this new revenue stream a reality the courses on finservMarketing will help.

Investment

Once again, we’ll categorize these expenses as investments to keep on track with the ROI theme but as a matter of business management, these are marketing & advertising, education, and service expenses.

T = Time

Your time is valuable and it certainly should be considered as should the time of any employee tasked with social media management on behalf of your firm. The one important note here, however, is to avoid over-allocation of time spend on social media as the cost associated with your business. Be efficient and purposeful with your efforts and consider only the costs of business activity.

Over the course of a year, you may spend, on average, 5 hours per week adding connections, scanning updates, reviewing alerts, publishing content, commenting and reaching out to prospects via social channels. Again, as a matter of practicality this time is no different than attending networking events, using email or making phone calls but for purposes of this exercise let’s quantify it.

In keeping with our simple theme let’s use an hourly rate of $100. Now I know a lot of top producers have effective hourly rates that are many multiples of this figure and that’s fine. If that’s the case you would also adjust the average client account size above in the "Revenue Per Client Annually” component as well.

At $100/hour and 5 hours a week spent on the business use of social media over the course of a 48 week work year your time investment would be $24,000 for the year.

P = Paid Marketing

As I mentioned at the beginning of the post, your business is dramatically different than many businesses using social media to attract customers. Your business is based on relationships. As a result, your expected paid marketing expense is likely to be very low compared to most businesses. Below are a few out of pocket expenses you will likely have as you begin to make social a priority in your practice:

- Social Media Management Solution - As a regulated professional you are going to need a solution that ensures your activity meets compliance standards. Social media activity of a business nature, like all electronic communication, must be archived for record keeping and be supervisable by appropriate management and your compliance team. There are several solutions available at a variety of price points depending on your business structure and firm affiliation. If you are an independent professional with full autonomy over your regulatory responsibilities you should explore HootSuite or RegEd’s Arkovi system. If you are affiliated with a larger firm that has compliance supervisory authority over your practice you will likely be using Hearsay or Actiance. The annual price for these solutions range from $100 to $500 per user for the year.

- LinkedIn Premium Account - Of the four major social networks, LinkedIn is the only one that offers premium solutions. You can get a lot done with a free account but there are a few features that make having a premium account worth it. Prices of premium accounts range from $100 to $900 per user per year.

- Social Media Advertising - While you can certainly feel free to experiment with ads on Facebook, LinkedIn and Twitter to increase your fans and followers, I’m not convinced this is the best investment for a financial professional at least in the early stages of building your practice. Once you have scaled your client base it may begin to make sense to take advantage of the social graph advertising options available on the major networks but you should expect your spend to be relatively low. Let’s say $1,200 a year for ads maybe. Note: Ads are also a challenge because they will need to be pre-reviewed by compliance.

Altogether you may have a maximum out of pocket spend of $2,600 for the year on paid marketing.

Ed - Education

I’d be remiss if I didn’t include this one.

The price of education is either paid through years of experience in trial and error or it’s paid in the form of hiring a professional who will share his knowledge, skills and wisdom. This is the value proposition of hiring a financial professional and it is the value proposition for finservMarketing as well.

Coming up to speed on social media marketing, and more broadly digital marketing, can take quite a bit of time. Our goal is to shorten that timeframe dramatically with easy to follow video tutorials and live webinars at a price point that is approachable for financial professionals at any stage of business development. We’ll take the guess work out of your social media marketing efforts and give you actionable strategies that produce results.

A year of finservMarketing courses might cost about $1,000, depending on how many courses you take.

Important Note: Your firm will likely require you to attend compliance training on the dos and don’ts of social media. If you operate an independent firm you should ensure all of your licensed professionals complete social media compliance training.

Investment Equation

Now let’s put together the investment (actually expense) side of the equation.

$24,000 Time + $2,600 Paid Marketing + $1,000 Education = $27,600 Investment

Key things to remember:

- The time expense is really a managerial accounting expense. Unless you hire an individual specifically for the task of managing your social media efforts this expense is not likely cash expenditure.

- This “investment” is a single year expenditure of effort and expense that generated the multi-year revenue stream above. Of course you will continue to invest in your social media marketing efforts in future years but in each year the investment/expense should be evaluated on their own merit.

Putting It All Together To Calculate Your ROI

($352,432 New Revenue - $27,600 Investment) / $27,600 Investment = 1,177% Return on Investment

That is is a pretty exciting number for any business. What makes it so realistic is the very nature of the business model of a modern financial professional. You build your business on relationships and as a matter of course traditional marketing expense is very low, compared to other businesses, while recurring revenue is the norm.

The numbers look pretty solid even if we only include the first year’s new revenue of $50,347. In that case, you would still realize an 82% ROI. As a general rule, if you produced an 82% return to your clients in a year they would be very happy customers.

Conclusion

The point of this in-depth exploration of social media ROI was to empower you with a process for evaluating social media usage for your business. Too often advisors, agents and wholesalers shrug off social as being a waste of time and not worthy of their attention. But as you discovered here, social is almost tailor-made for the way financial professionals do business.

If you have questions or would like to dig a little deeper on this or any other topic please let me know. I would love to hear your thoughts in the comments below.

How to Shorten the Sales Cycle for Financial Advisors and Insurance Agents

There is a big challenge that every financial advisor and insurance agent is likely to face in building a practice. It's a challenge that few people in the industry talk about yet it is one of the most significant factors contributing to the high washout rates for new professionals entering the financial services field.

The sales cycles for financial advisors and insurance agents is very long.

It is not uncommon for it to take several months or even a few years to convert a prospect to a client. To a person who has never been a financial advisor or an agent this may seem absurd but the reality is there are real fundamental reasons for why it takes so long to bring on new client relationships. Some of these reasons are structural in nature and beyond the control of the advisor or agent but others are easily manageable by employing new processes and leveraging the wealth of digital solutions available to modern financial professionals.

The goal of this post is to help financial professionals (and the broker-dealers, wire houses, and insurance carriers who rely on these individuals) dramatically shorten the time it takes to create a profitable and sustainable book of business.

To get a better idea of what an advisor or agent can do to speed things up let's break down some of the factors contributing to the long sales cycle for new financial clients.

Structural Reasons for Long Sales Cycles - Limited Control Items

- Booking the Initial Meeting - Oh for the good old days where rooms full of stockbrokers where making cold calls to sell prospects on the latest hot stock that they just had to get in on before it skyrockets. Things were much easier then. No need to schedule a meeting to talk to the prospect about his goals and risk tolerance and so on. Build a relationship?! Relationships were built on picking good stocks. The world is different now. Advisors and agents need to meet with a prospect first to explore their needs. To make matters worse, affluent and wealthy prospects are typically very busy and it can take weeks to get on their calendar.

- Developing a Plan - Once the initial meeting has taken place the financial professional needs to plug everything he's learned into the system and craft a plan that fits the prospect's needs and goals. Technology has already made this process pretty quick but you can still expect it to take a few days and revisions.

- Booking the Follow Up Meeting - Ideally this meeting was scheduled at the conclusion of the initial meeting. Remember this phrase "book a meeting from the meeting" never leave the prospect without knowing when you'll see him or her next. Like the initial meeting, this can take weeks and it isn't uncommon for it to be rescheduled.

- Booking a Second Follow Up Meeting -This happens more often than any financial professional would like to admit. The prospect wants to explore adjusting the plan or has also met with a competing advisor or any number of other reasons. The best thing to do in this situation is learn from it. Pay close attention to why this meeting is happening at all. If it is something fixable in the process be sure to fix it.

- Application Processing Time - This is getting shorter but there is still an insane amount of paperwork required to establish a new account, initiate a transfer or assets (TOA) or rollover request, set up electronic bank transfers and then comes the waiting for funds to clear once the dust settles. If you are lucky and there's a reasonable amount of electronic exchange of information you might see the relationship established within 10 days. Of course if there is a form returned as NIGO (not in good order) or there is a 401(k) rollover that needs to be processed it could be over a month.

- Underwriting Time - New life insurance policies or long-term care coverage? Wow! That's going to take a couple of months.

Process Reasons for Long Sales Cycles - Controllable Items

- Life Events Dictate Timing - Not everyone an advisor or agents meets is in the market for his services right now. Eventually many people will be. Unfortunately, there's really no way of know when "eventually" will happen. The affluent Senior Vice President an advisor meets today may stay at her at her current company for another five years. That means she won't be ready to rollover her $1 million dollar 401k account until then. If she could she certainly give the advisor her business but at the moment she has relatively little in the way of investible assets. There are few things to do here to improve the overall sales cycle:

- Increase Your Pool of Prospects - Think of this process as being similar to creating a bond ladder. Only this ladder is a bit random in nature. Not every prospect is going to mature into a client at the same time. So, the trick is to have a lot of prospects in the mix.

- Stay Connected - Losing touch with a quality prospect is like losing touch with tens of thousands of dollars. It should never happen. Staying connect means you will always be at the top of the prospect's consideration set for their business in the future. It also means you aren't leaving things to chance. You should know when that SVP you met five years ago changes jobs.

- Take Their Small Business Now - If you have identified a high potential prospect find a way to make them a client now. Why leave the future up to chance? Aren't client relationships supposed to be lifelong? If you think this client is going to grow over the years why not lock them up now? Many firms have asset minimums and that makes sense on an ongoing basis but if there is a case where you have a high degree of confidence that a prospect will grow into the asset minimum in the not too distant future...bring the client on.

- Lack of a Target Market - The first course we produced on finservMarketing is focused on the importance of having a target market. Every business in the world needs to be able to answer the question "Who is your customer?" and yet the majority of financial advisors and insurance agents have given the notion little thought. As a result their marketing efforts are random and generalist in nature. The most successful financial professionals know exactly who they are looking for and their entire business is designed to serve that client niche. Having a well defined target market makes everything about your business more efficient. Including your sales cycle.

The most important things a financial professional can do to shorten the sales cycle in his practice are to develop a target market, spend a lot of time developing prospects within that target market, and get really good at managing the meeting and onboarding process. As his practice matures it will develop a momentum of its own and sales cycle time will be less of a concern. But until then, every effort should be made to speed things up.